End of an Era: A Big Change Underway

“I finally know what distinguishes man from the other beasts: financial worries.” – Jules Renard, French Author (1864-1910).

When the stock market goes down, we wonder much how lower it can go.

When it goes up, we wonder if we’ve reached a market top.

Wonder, is the name of our game.

Even if the result of the US presidential election were different, the title of my last newsletter for 2016 would be same.

There are some significant changes in long term trends coming our way. I will discuss what those trend reversals are and what they may mean for your investments.

But first things first: I wish you a pleasant Holiday Season and hope that 2017 brings peace, health and prosperity to us all.

Reversal of Long Term Trends

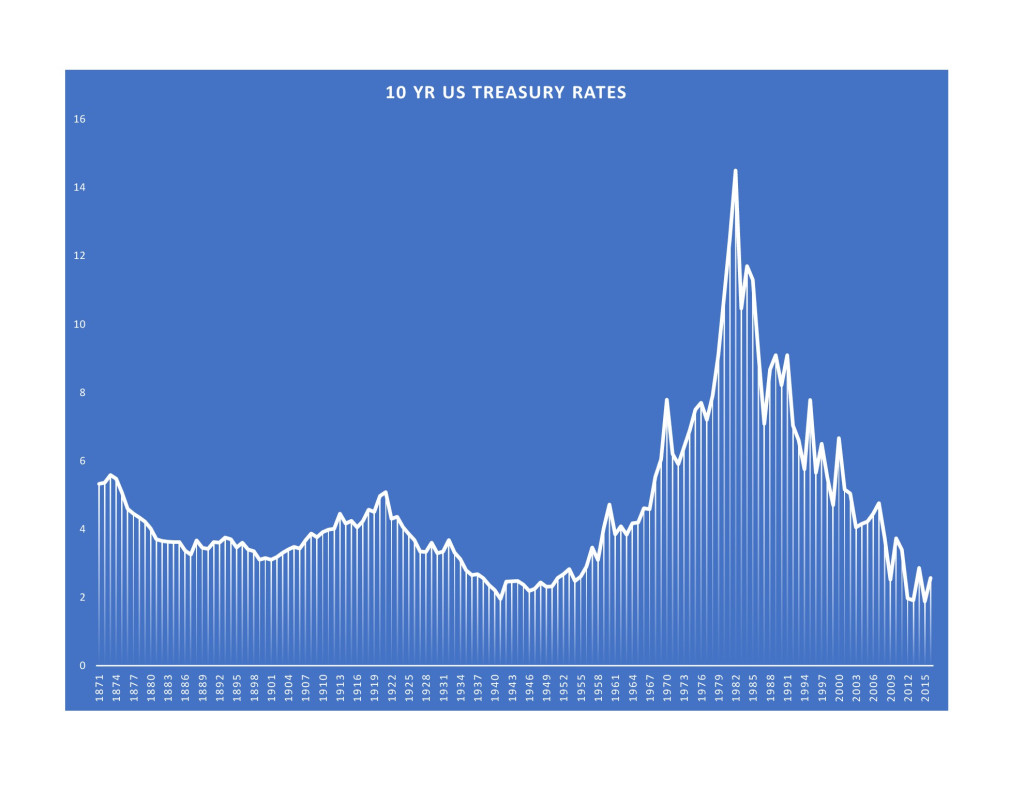

A picture is worth a thousand words, please see 10 Year US Treasury long term chart going back to 1800s.

Please note that the current rise in interest rates is coming off of a base that was last seen during WWII. Bond yields have been in a steady downtrend since 1982. A 5% bond becomes more attractive when new issues pay 4%, and so it gets a premium. This inverse relationship between bond prices and yields has created a 34-year bond bull market since 1982. It is also important to note that the length of the previous bond bear market was 36 years, so I think this much is fair to say; a long-term trend might be in a reversal mode and when it reverses, it may stay there for a very long time. Just when the FED has completed its monetary easing tactics, and was getting ready to take back the punch bowl, something else also had happened: the US presidential election.

Many experts, including the FED itself, have been underlining the diminishing returns in monetary easing policies. In fact, the FED has been complaining about Congress falling short of doing its part in fiscal expansion to stimulate growth and fight deflation.

The unfortunate reality about US politics, is that it has been very difficult for a Democratic Party president and its administration to borrow and spend in this current environment, for two reasons: 1- It is a shared government with a Republican Congress and these efforts get blocked 2 – They are easily labeled as a road to big government and get a push back.

But with the Republican Party holding executive powers, especially with the tailwind created by the disgruntled masses demanding change, along with a Republican Congress, fiscal expansion is now the writing on the wall.

Add them together, this end of monetary easing and the beginning of fiscal expansion, and you get a rising rate environment. This shift will likely become the catalyst for our third big change: falling bond prices.

Although they are interconnected, these developments create some separately affected winners and losers.

For instance, a rising interest rate environment usually hurts stocks…but probably not this time, for three reasons: 1 – Rates are so low, current increase doesn’t pose a threat, just yet. 2 – It also signals the strength of the underlying economy. 3 – And most importantly, it may kick-start the long awaited “Grand Rotation” from bonds to stocks.

To recap, these four big events, 1 – End of monetary easing 2 – Rising interest rates 3 – Beginning of fiscal expansion and 4 – Great Rotation from bonds to stocks, signify the end of an era.

The side effects of this can be a strong dollar, rising equity prices and valuations, and a drop in residential real estate prices. These side effects, though they make sense, may be limited in size and/or occur at a moderate pace.

Moving on to our next big change item; tax cuts, both at the corporate and personal levels.

Corporate tax rates haven’t moved much, at least in a meaningful way since 2000. To be fair, after the 2008 Global Financial Crisis, the Obama administration allowed corporations to deduct their losses from their current profits with a look back period of 5 years. This essentially created a tax cut for corporations, and contributed to an unprecedented profit growth.

Now, a real and significant tax cut may be under way, and I hate to put it this way but otherwise it could be a tough year for US corporations. A stronger dollar can hurt exporters, which most large US corporations are. Rising interest rates increase the cost of borrowing, and if you’re wondering why the US stocks have been going up since the election, along with the reasons mentioned above, the expectation is that a tax cut would more than compensate for these headwinds.

The same can be said about personal income taxes. The top tax bracket has seen an increase in the last few years but a tiny portion of the US population is subject to it. In fact, 50% of the tax payers don’t pay Federal Income Tax (but they do pay FICA taxes).

So, a tax cut would be a game changer depending on how it’s structured. Not all tax cuts are created equal. Someone making $35,000 a year, will likely spend a majority of the additional (marginal) cash that he/she receives. Conversely, someone making a million dollars year, will save a majority of the additional funds he/she receives. This dichotomy creates vastly different end results with tax policies…hence, the reason for all the heated discussions. Also, let’s not forget, lower tax rates mean a lower federal budget and larger deficits, unless of course, the growth it stimulates makes up for it…which is a whole other discussion.

Last, but not the least big change item worth mentioning, is the inflation rate. I think after years of being fearful of deflation, we might start observing some mild increase in the inflation rate which, at these extremely low levels, is not a red flag by any means but rather a significant change.

Your Investments

If one would take all this into consideration and form an actionable investment strategy, what would surface to the top? In my opinion, these areas may benefit from the above trends:

- Small and mid-size company stocks with limited export exposure.

- Large companies with cash stock piles, as the borrowing costs may start going up.

- Industrial stocks may benefit from the infrastructure spending and capital expenditures, where the bulk of the fiscal spending may end up.

- Tech sector, especially semi-conductors may benefit, as this sector gets a boost from capital expenditures.

- Bank stocks, especially local banks may be the prime beneficiaries of a rising rate environment.

- Energy stocks may get a boost, as they present one of the few areas of value in the market and benefit from a stabilizing oil price.

- Consumer stocks, as tax cuts may boost consumption.

- On the flip side of the coin, treasury bonds, especially those with long duration may see their values drop, so look for bonds that would be the least affected by rising rates, such as convertibles or inflation linked.

- Lastly, be watchful of international investments and when you can, look for dollar hedged choices, as a rising dollar may hinder returns from returns from overseas.

- Real estate prices may be flat or in a downtrend, as the mortgage rates have already started to go up, unless of course deregulation of this industry attracts newer demand.

It is always a fool’s errand to predict the future, but it is my job to take a shot at it. I hope my calculated guesses have presented an informative and interesting read for you.

Disclosure

The strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. There is no guarantee that any strategies discussed will be effective. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy.

The information provided is not intended to be a tax advice. Investors should be urged to consult their tax professional or financial advisers for more information regarding their specific tax situations.

Featured News & Insights

- January Market Commentary

- 2026 Global Market Outlook

- December Market Commentary

- November Market Commentary

- October Market Commentary

- September Market Commentary

- July Market Commentary

- 5 Smart Investment Moves During Market Downturns

- Preparing for 2024 Tax Filing: A Comprehensive Roadmap to Your Tax Documentation

- A New Regime Comes Into Focus

- Important New Filing Requirement for Entity involvement

- Property Alert Services

- You are being targeted by Search engine optimization (SEO) scams.

- Navigating the Tax Maze: A Comprehensive Guide to Documenting Your 2023 Tax Return

- December Market Commentary Rates: Lower and Sooner?

- What Issues Should I Consider Before The End Of The Year 2023

- A Raft of Reassuring Data – or Not?

- Guarding Your Financial Future: The Power of Credit Freezing

- Deglobalization and Dedollarization

- Debt Deadlines, Defaults and Downgrades

- What Issues to Consider as my child becomes independent

- Estate Planning

- Tax Season Help Has Arrived

- 2023 Outlook

- Inflation Impacts

- Should a Trust Be Part of Your Estate Plan?

- How to Have “The Talk” With Your Aging Parents

- The psychology of retirement

- The Optimal Retirement Withdrawal Plan

- Avoiding the Big Mistake

- The Overlooked Key to Estate Planning Success: The Psychology of Communication

- Higher and Faster: The Fed Turns Up the Heat

- Taxes FAQ 2022

- Four Steps to Cope with Market Madness

- The Russian Invasion of Ukraine

- Five Questions to Ask Before Investing in Crypto

- April 2021 Newsletter

- 5 Tips for loving life in tough economic times

- Once Again, It’s the End of the World

- Are Investors Their Own Worst Enemy?

- Charitable Giving: Beyond the Basics

- 2019…And the Plot Thickens

- Oil Falls, Dollar Rises, Stocks Get Confused